New Jersey Real Estate & Economic Trends: Analysis for Spring 2025

I. Introduction

Purpose: This report provides an expert analysis of the key developments influencing the New Jersey real estate market, the interconnected U.S. housing economy, and mortgage interest rates during the period of mid-February to mid-April 2025. It synthesizes recent data, news reports, and expert commentary to offer a clear overview for stakeholders navigating the current market landscape.

Context: The timeframe examined captures the typical ramp-up of the spring real estate season. However, this seasonal activity occurred against a backdrop of significant economic crosscurrents. While mortgage rates showed some easing from earlier peaks, they remained elevated compared to recent years. Persistent inflation concerns, coupled with considerable uncertainty surrounding federal economic policies, particularly tariffs, shaped market sentiment and activity during this period.

Interconnectedness: It is crucial to understand that the New Jersey real estate market does not operate in isolation. Its performance is intrinsically linked to the health of the broader U.S. economy, including factors like inflation, employment trends, and GDP growth, which influence housing demand and supply nationally. Furthermore, federal policies, such as those enacted by the Federal Reserve regarding interest rates and potential trade tariffs, exert significant influence. Financial market conditions, particularly the behavior of U.S. Treasury yields and the resulting mortgage interest rates, directly impact housing affordability and buyer activity in the state.

Scope: This analysis focuses specifically on news and data relevant to the New Jersey real estate market (including home prices, inventory levels, and sales activity), the U.S. economy's impact on the national housing market, and mortgage interest rate trends (including recent changes and forecasts) published between mid-February 2025 and mid-April 2025.

II. Key News Summaries & Analysis (Mid-February to Mid-April 2025)

A. NJ Spring Market Awakens: Activity Surges, But Inventory and Price Hurdles Persist

The arrival of spring 2025 brought a noticeable surge in activity to the New Jersey and broader Mid-Atlantic real estate markets, consistent with seasonal patterns. Data from March indicated a significant month-over-month increase in market velocity. Across the Bright MLS service area, which includes parts of New Jersey, new pending sales jumped 37.5% between February and March, alongside a 38.5% rise in new listings entering the market. Showing activity, a measure of buyer interest, also surged by 39.5% month-over-month. The Philadelphia metropolitan area, encompassing several South Jersey counties, mirrored this trend with a 41.1% month-over-month increase in pending sales and a 33.0% rise in new listings. Statewide New Jersey data corroborated this trend, showing a 10.9% increase in active listings from February to March, with every county experiencing a double-digit percentage increase in new listings month-over-month. Year-over-year comparisons also showed improvement, with active listings up 14.57% statewide compared to March 2024 and new listings up 12.6% across the Bright MLS area.

This increased activity translated into a faster pace of sales in March compared to the preceding month. The typical home in the Bright MLS service area went under contract in just 12 days, seven days quicker than in February. Similarly, statewide data indicated homes typically stayed on the market for 33 days in March, a 25% reduction in time compared to February. However, this pace was slightly slower than the previous year; March's median days on market was two days slower than March 2024 in the Bright MLS area , and February 2025 saw homes staying on the market slightly longer than in February 2024 across New Jersey (e.g., 48 vs 44 days statewide , 56 vs 51 days for single-family homes in Ocean County , and 74 days in the South Jersey Shore ).

Despite the surge in listings and activity, home prices continued their upward trajectory, underscoring persistent demand. The median listing price in New Jersey reached $550,000 in March, a modest increase both month-over-month (0.93%) and year-over-year (0.18%). Other sources confirmed this trend: Zillow reported the average New Jersey home value at $542,608 as of February 28, up 7.2% over the past year , while Redfin noted a 9.2% year-over-year price increase in February. The median sold price in the Bright MLS area was $410,000 in March, up 4.1% year-over-year. Specific segments within New Jersey also saw significant gains earlier in the period; February data showed the median sales price for single-family homes statewide jumped 13% year-over-year to $565,000 , while Ocean County saw median prices rise 1.4% for single-family homes and 10.8% for condos year-over-year.

Crucially, the increased spring activity did not resolve the underlying inventory shortage. While listings rose in March, overall supply remained constrained. The Bright MLS service area still had less than two months of housing supply in March , significantly below the four to six months typically considered a balanced market. February data indicated statewide single-family listings were down 3% year-over-year, fostering tight competition. Even in the Philadelphia area, active listings at the end of March remained less than half of what they were in 2019. The South Jersey Shore reported 3.6 months of inventory in February, an improvement over the prior year but still indicative of limited supply. This local scarcity reflects a broader national housing deficit, estimated at 3.7 million homes , and contributes to New Jersey battling a persistent lack of overall inventory.

The confluence of these factors—a seasonal activity surge driven partly by slightly lower mortgage rates , coupled with persistently low inventory levels and continued price appreciation—suggests that the spring awakening primarily reflects pent-up demand and supply responding to marginal improvements and seasonal timing, rather than a fundamental shift towards a balanced market. The underlying supply constraints remain significant. Furthermore, the fact that prices continued to climb even as more listings became available highlights the strength of buyer demand, which appears robust enough to absorb new inventory quickly while still driving prices upward. This competitive pressure is further evidenced by reports of homes selling for slightly above their list price, such as the 101.3% median sale-to-list price ratio reported for New Jersey in January and noted as a trend in February.

Note: Data reflects various sources and time points within the Feb-Apr 2025 period. MoM = Month-over-Month; YoY = Year-over-Year. Bright MLS includes parts of NJ, PA, DE, MD, VA, WV, DC. Philly Metro includes parts of NJ & PA.

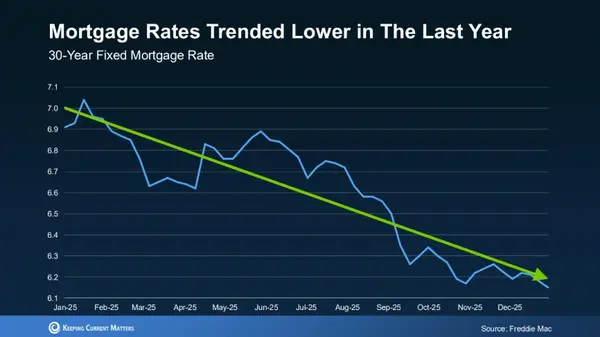

B. Mortgage Rates Dip Below 7%, Offering Slight Reprieve, But Affordability Crisis Looms Large

During late March and early April 2025, mortgage rates exhibited a modest downward trend, offering a sliver of relief to prospective homebuyers. Data from Freddie Mac indicated that the average rate on a 30-year fixed-rate mortgage declined for three consecutive weeks, falling to 6.62% by April 10. This marked twelve consecutive weeks where the average remained below the 7% threshold. Other sources reported similar levels, with Bankrate's survey showing an average of 6.76% on March 26 and New Jersey-specific rates averaging 6.79% for a 30-year fixed loan as of April 10. While daily fluctuations occurred , the general trend provided a marginal improvement in borrowing costs compared to earlier in the year when rates briefly exceeded 7%.

This easing, however slight, appeared to stimulate some market activity. Declining rates were credited with boosting homebuyers' purchasing power and enticing some buyers back into the market, contributing to the spring activity surge. Purchase application demand saw increases during periods of rate stability or decline.

Despite these incremental improvements, the overarching narrative remained one of severely constrained housing affordability. Mortgage rates, while below recent peaks, were still substantially higher than the historically low levels seen during the pandemic era and remained elevated compared to long-term averages. This sustained high cost of borrowing, combined with record-high home prices , continued to suppress overall housing demand and presented significant affordability challenges for many households. The reality for many was stark: a six-figure annual income was reportedly necessary to afford a median-priced home in New Jersey and numerous other states. High housing costs stalled the plans of many potential buyers , and even with rates dipping, the elevated home prices meant that the overall cost of buying was not becoming substantially cheaper.

Looking ahead, expert forecasts consistently suggested that mortgage rates would likely remain in the mid-to-high 6% range for the remainder of 2025. Projections for the second quarter of 2025 averaged around 6.66%, with forecasts ranging from 6.5% to 6.8%. End-of-year 2025 forecasts generally anticipated rates hovering around the mid-6% mark, perhaps easing slightly towards 6.5% or 6.7%. Analysts predicted rates would likely stay within a 6.5% to 7% band through April and potentially a 6.5% to 7.25% range for most of the year. Achieving rates below 6% appeared improbable without a significant economic downturn.

The trajectory of mortgage rates is tied to a complex set of factors. Rates closely track the yield on 10-year U.S. Treasury notes. These yields, in turn, are influenced by investor expectations about future inflation , the Federal Reserve's monetary policy decisions (particularly regarding the federal funds rate) , incoming economic data such as jobs reports and consumer spending figures , and broader global economic uncertainty, including the potential impact of trade tariffs.

Table 2: Mortgage Rate Forecast Summary: Q2 2025 - End of 2025 (Average 30-Year Fixed)

| Forecasting Authority / Expert Source | Q2 2025 Forecast | End-of-Year 2025 Forecast | Source(s) |

|---|---|---|---|

| National Association of Realtors (NAR) | 6.50% | ~6.5% (Implied by Q4) | |

| Wells Fargo | 6.55% | N/A | |

| Nat. Assoc. of Home Builders (NAHB) | 6.65% | N/A | |

| Fannie Mae | 6.80% | 6.3% | |

| Mortgage Bankers Association (MBA) | 6.80% | 6.5% | |

| Average of Q2 Forecasts | 6.66% | ||

| Freddie Mac (General Outlook) | ~6.5% for year | ~6.5% for year | |

| J.P. Morgan Research | N/A | Easing slightly to 6.7% | |

| Bright MLS Economist (Sturtevant) | N/A | Mid-6% range for much of year | |

| Other Expert Consensus (Various) | 6.5% - 7.0% (April) | Mid-6% range |

Note: Forecasts are subject to change based on evolving economic conditions. N/A indicates forecast not specified for that period in the reviewed sources.

C. Economic Uncertainty Clouds Outlook: Recession Fears, Inflation, and Tariffs Influence Market Sentiment

A palpable sense of economic uncertainty permeated the housing market discussion during mid-February to mid-April 2025. Concerns revolved around three primary interconnected issues: the potential for an economic recession, the persistence of inflation, and the unpredictable impact of U.S. trade tariffs. These factors collectively contributed to market volatility and influenced the confidence of consumers and businesses alike.

The prospect of a recession in 2025 was a recurring theme in economic commentary, with some economists estimating a significant likelihood. Warnings emerged that weakening economic conditions could dampen the typical spring housing market surge. A recessionary environment would likely lead to increased unemployment, reduced buyer demand, slower home sales, rising inventory, and downward pressure on prices. While some argued the housing market had limited room to fall further given already low sales volume , the potential for job losses remained a primary concern.

Inflation, although showing signs of moderation from peak levels , remained stubbornly above the Federal Reserve's target. Shelter costs, a major component of inflation indices, continued to rise, albeit at a slower pace. This persistent inflation kept the Federal Reserve cautious about lowering interest rates , thereby keeping borrowing costs elevated.

Perhaps the most significant source of immediate uncertainty during this period stemmed from the Trump administration's actions and rhetoric regarding international trade tariffs. These tariffs were widely seen as a risk factor with multiple potential negative consequences for the housing market and the broader economy. Concerns included:

- Increased Inflation: Tariffs on imported goods could push up consumer prices, potentially counteracting efforts to control inflation and prompting higher interest rates.

- Higher Construction Costs: Tariffs on materials like lumber and appliances could increase the cost of building new homes, impacting affordability and potentially slowing construction.

- Market Volatility: Tariff announcements triggered immediate reactions in financial markets, leading to stock market declines and fluctuations in bond yields, which directly influence mortgage rates.

- Economic Slowdown: Retaliation from other countries and disruptions to global trade raised fears of a broader economic slowdown or even recession.

This confluence of recession fears, inflation persistence, and tariff uncertainty weighed heavily on consumer sentiment. Reports noted declining consumer confidence and growing anxiety among the public. Such uncertainty makes prospective homebuyers hesitant, unsure about future economic stability and the direction of mortgage rates. The fear of potential job loss in an economic downturn could easily outweigh the appeal of potentially lower mortgage rates that might accompany a recession.

The housing market during this period was thus caught in a complex dynamic. Factors that might traditionally push mortgage rates lower, such as signs of economic weakness or recessionary fears leading to a "flight to safety" into bonds , were being counteracted by inflationary pressures, partly fueled by tariff concerns, which argued for higher rates or Fed caution. This tension created significant volatility and made forecasting rate movements particularly challenging. Beyond the direct economic effects, the sheer uncertainty surrounding policy, especially tariffs, acted as a drag on the market. It fostered a "wait-and-see" attitude among some buyers, sellers, and builders, delaying decisions and potentially freezing activity irrespective of immediate cost implications. While a recession could theoretically improve affordability through lower prices and rates, the associated risks of job loss and potentially tighter lending standards mean that such an "improvement" might not be accessible or beneficial for many households, particularly those most affected by the economic downturn.

D. National Inventory Shows Signs of Life, But NJ Remains a Competitive Seller's Market

Examining housing inventory reveals a divergence between national trends and the specific conditions within New Jersey. Nationally, there were indications of supply beginning to recover during the early months of 2025. The number of existing homes for sale saw year-over-year increases in February and March. New home construction also showed positive signs, with an 11.5% increase in February and forecasts predicting 1.1 million new homes built in 2025, a 14% increase over 2024. Inventories of new homes for sale reached their highest levels since 2007-2008. Some analyses suggested that inventory levels in the South and West regions of the U.S. were approaching pre-pandemic averages. To move this growing inventory, some builders were reportedly offering incentives like mortgage rate buydowns and closing cost credits.

However, this national picture contrasted sharply with the situation in New Jersey. Despite the statewide surge in new listings during March , the overall level of available housing inventory remained exceptionally tight relative to demand. As noted earlier, months of supply hovered well below balanced market levels across the state and its subregions. New Jersey continued to be characterized as a market battling a fundamental lack of inventory , keeping competition high among buyers. This aligns with broader regional trends; data indicated that inventory in the Northeast remained significantly depressed compared to pre-pandemic levels, down 57.5% as of March, far more constrained than the South or West.

Consequently, despite seasonal improvements, the New Jersey housing market largely retained its character as favoring sellers. The low supply levels ensured that demand continued to outstrip the available homes, supporting prices and maintaining a competitive environment. While some stabilization was noted in specific areas like the South Jersey Shore , the overall state picture was one of imbalance. A significant factor contributing to this persistent low supply is the "lock-in effect," where a large majority of existing homeowners hold mortgages with interest rates significantly below current market rates (often below 4%), making them reluctant to sell and give up their favorable financing. This drastically reduces the turnover of existing homes, which is a crucial component of housing supply.

Therefore, the notable increase in New Jersey listings observed in March should be interpreted with caution. It represents a welcome seasonal uptick within a market that remains fundamentally undersupplied, reflecting the broader constraints seen across the Northeast rather than mirroring the more substantial inventory recovery observed nationally or in other regions. The deep-seated inventory shortage in New Jersey appears driven by a combination of factors, including potentially slower regional new construction recovery compared to other areas and the powerful impact of the mortgage rate lock-in effect limiting existing home sales. Furthermore, the national increase in new home inventory may offer only limited relief in many parts of New Jersey, particularly the densely populated northern and central regions where land suitable for large-scale development is scarce and expensive. While multifamily construction has seen demand , the state's overall inventory challenges likely depend more heavily on unlocking the existing housing stock rather than solely relying on the national surge in new single-family construction.

E. Navigating the Market: Strategic Considerations for NJ Buyers and Sellers in Spring 2025

The market conditions observed between mid-February and mid-April 2025—characterized by a seasonal activity surge, easing but still-high mortgage rates, persistent price pressures, low inventory, and significant economic uncertainty—presented a complex landscape for both buyers and sellers in New Jersey. Navigating this environment required strategic planning and careful consideration.

For Prospective Buyers: The spring market offered slightly more choice than the winter months due to the increase in listings. However, competition remained intense. Key considerations included:

- Preparation and Speed: With homes selling relatively quickly and demand strong , being pre-approved for a mortgage was essential to making a competitive offer. Buyers needed to be prepared to act decisively when finding a suitable property and utilize tools like new listing alerts.

- Managing Competition: Buyers should anticipate potentially competing against multiple offers and be prepared for homes selling above the asking price. Working with an experienced local agent to understand market dynamics and craft a strong offer strategy was advised.

- Leveraging Market Nuances: While still competitive, the slight increase in inventory and marginally slower year-over-year sales pace in some segments might have offered slightly more room for negotiation compared to the peak frenzy, particularly in areas showing signs of stabilization.

- Financial Strategy: Diligently shopping for the best mortgage rate from multiple lenders was important. Exploring options like seller-paid buydowns could also help mitigate high rates. Locking in a favorable rate quickly was recommended.

- Flexibility and Creativity: Given high prices, exploring emerging neighborhoods or considering properties requiring some work might be necessary. Creative offer terms, such as offering a flexible closing date, could sometimes strengthen an offer without increasing the price.

- Risk Assessment: Buyers needed to weigh the potential benefits of slightly lower rates against the risks posed by economic uncertainty, potential job insecurity in a downturn, and the possibility of buying near a price peak.

For Prospective Sellers: The market continued to offer favorable conditions for sellers in many parts of New Jersey , allowing them to capitalize on high home values. However, strategic positioning was becoming increasingly important:

- Pricing Accuracy: While demand was strong, overpricing could lead to significantly longer times on the market. Strategic pricing aimed at attracting broad interest and potentially generating multiple offers was key. Sellers also needed to consider the financial stability of potential buyers when evaluating offers.

- Optimal Timing: Spring and summer are traditionally peak selling seasons , and the March data confirmed the market was ramping up. Listing during this period could maximize exposure to active buyers.

- Addressing Competition: The increase in spring listings meant sellers faced more competition than during the winter months. Ensuring the home was well-prepared and effectively marketed was crucial to stand out.

- Condition Matters: To justify high asking prices in a market where buyers might be feeling financial pressure, ensuring the home was in top condition was essential.

The central challenge for buyers during this period was balancing the urge to act quickly amidst competition and slightly improved conditions against the significant risks associated with high prices and economic headwinds. Making a decisive move was often necessary, but careful financial assessment to avoid overstretching budgets was paramount. For sellers, while the market remained advantageous, the landscape suggested that complacency was ill-advised. The modest rise in inventory and prevailing economic caution meant that thoughtful pricing, excellent property presentation, and strategic marketing were becoming more critical differentiators compared to the absolute peak of the seller's market frenzy. Careful positioning was necessary to maximize returns and ensure a timely sale.

III. Concluding Remarks

The New Jersey real estate market between mid-February and mid-April 2025 presented a dynamic but challenging environment. The traditional spring surge in activity was evident, with more homes listed and sold compared to the preceding months. However, this seasonal energy was significantly tempered by persistent headwinds: housing affordability remained near historic lows due to the combination of high home prices and mortgage rates hovering in the mid-to-high 6% range, while overall inventory levels stayed stubbornly low, particularly for existing homes.

Overlaying these market-specific factors was a considerable degree of economic uncertainty. Concerns about inflation, the potential for a recession, and the unpredictable effects of U.S. trade tariffs created volatility in financial markets, influenced mortgage rate movements, and impacted consumer confidence. The analysis underscores the tight linkage between local New Jersey market conditions, the trajectory of the national economy, and fluctuations in the financial sphere, particularly mortgage rates.

Looking forward, the interplay of these forces suggests continued market complexity. While mortgage rates may gradually ease further, substantial relief appears unlikely in the near term without significant shifts in economic fundamentals or policy. The inventory situation, particularly in densely populated New Jersey, remains a critical constraint unlikely to be resolved quickly. Therefore, stakeholders—whether buying, selling, or investing—must continue to monitor key economic indicators (inflation, employment), policy developments (Federal Reserve actions, tariff implementations), and local market data (listing trends, price changes, days on market) closely. Consulting with knowledgeable local real estate and financial professionals remains essential for making informed decisions in this fluid environment.

Categories

Recent Posts

GET MORE INFORMATION